Empowerment Economics: The Solvency Playbook—Turning Liquidity into Legacy

Cecil J. Lipscomb

When the economy tightens and inflation eats quietly from the edges of every ledger, clarity—not capital—becomes the great separator.

For small and midsized businesses and nonprofits, solvency is not about surviving the storm; it’s about building vessels strong enough to sail through it.

We can’t control inflation or currency volatility. But we can control the structure, strategy, and stewardship of our internal financial systems.

This is Empowerment Economics in practice: turning liquidity into legacy.

1. Liquidity Is Leadership—But Inflation Is a Threat

Every dollar you hold is slowly losing value. The logic of “cash is king” only works when that cash has a job to do.

Modern financial resilience comes from precision liquidity—keeping enough accessible funds for operational control without letting inflation and opportunity cost quietly erode their worth.

Best‑practice reserves for healthy organizations across the country show a pattern:

Nonprofits: 3–6 months of operating expenses held in unrestricted liquid reserves when income is stable; 6–12 months when reliant on seasonal or government funding.

Small and mid‑sized businesses: Typically maintain 10–20 % of annual revenue as working cash, scaling up during volatility.

Cash diversification: High‑yield business savings, insured money‑market accounts, and short‑term Treasury ladders balance liquidity and inflation protection.

Liquidity buys time, but unproductive cash loses value. The goal is availability with intention—not accumulation without return.

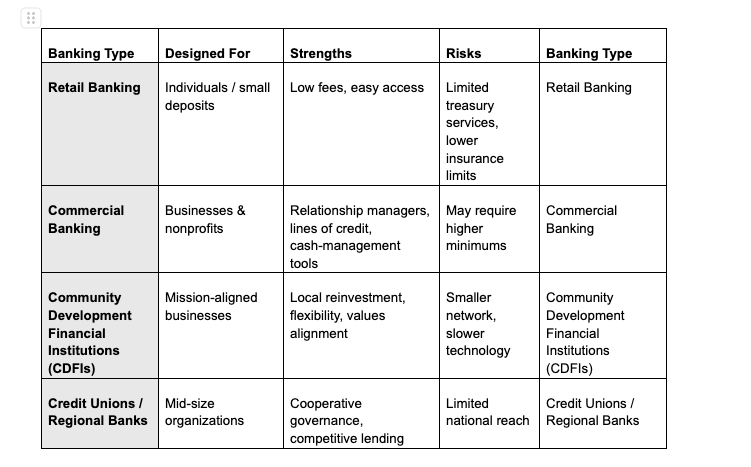

2. Beyond the Bank—Diversifying Financial Relationships

Too many local institutions keep all their funds in one bank—often a retail account intended for households, not enterprises. That’s risk disguised as convenience.

Understanding the difference matters:

Healthy organizations maintain two to three active institutional relationships—one for operational cash flow, one for reserves or treasury services, and one for investment custodianship. This diversification protects against liquidity freezes, bank‑specific crises, and service failures.

Banking isn’t neutrality; it’s alignment. Your depository partners should mirror your mission.

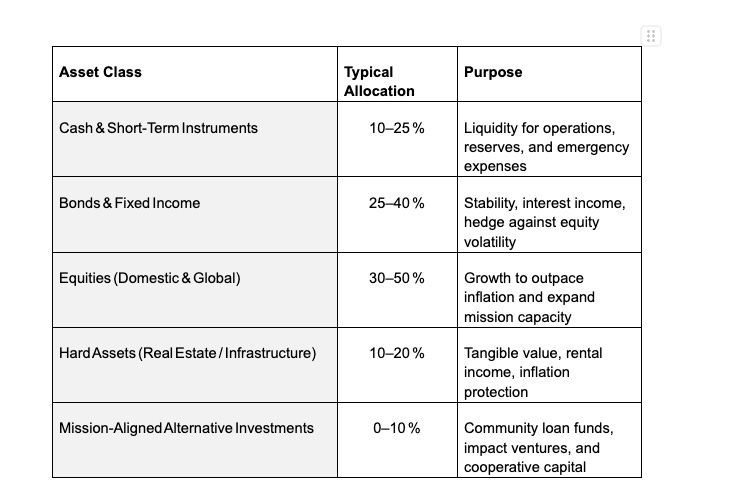

3. From Rainy‑Day Money to Investment Strategy

Inflation diminishes static cash, but investment multiplies mission when guided by disciplined allocation.

A balanced institutional approach might look like this:

These ratios vary, but the principle stands: resilient organizations invest across time horizons—cash for today, fixed income for the mid‑term, equities and real assets for the future.

Importantly, any nonprofit or mid‑sized enterprise with consistent surpluses should maintain its own institutional investment account rather than leaving funds idle in checking. This ensures professional oversight, transparent reporting, and compound growth guided by board policy.

4. Asset Stewardship—The Discipline of Permanence

Asset management is not only a finance function; it is a moral one.

It requires a living inventory of everything that carries value—cash, property, technology, intellectual capital—and the discipline to reinvest gains into mission‑critical assets.

Leading organizations model this by:

Adopting Investment Policy Statements (IPS) that define risk tolerance, liquidity needs, and ethical alignment.

Scheduling quarterly asset audits and valuation reports.

Incorporating real‑estate or equipment reserves into budgets for replacement or repair.

Using mission‑aligned investing—placing surplus funds in community loan pools or green bonds to serve both financial and social goals.

Sustainability is not only surviving lean seasons; it’s expanding responsibly when others retreat.

5. Endurance by Design

Economic cycles will continue. Costs will rise. Inflation will whisper through every line item. Yet organizations that treat solvency as strategy, not happenstance, will stand firm.

The playbook is straightforward:

Hold smart liquidity—3–6 months, not years.

Diversify banking relationships and investment classes.

Transform excess cash into purpose‑driven capital through disciplined allocation.

Manage assets as if permanence were policy.

Liquidity without leadership drains value. Leadership without structure burns it. Together they become permanent—the capacity to meet needs today without compromising tomorrow.

Empowerment Economics is no longer about survival at the margins; it’s about ownership at the core. The movement isn’t asking for charity—it’s designing solvency, stewardship, and power on purpose.